If the saying “everything in the universe is either growing or dying” applies to financial services, some traditional banks and credit unions — of all sizes — may be in their last days. That’s the sobering conclusion reached by banking analysts at Boston Consulting Group.

In its 2021 Global Retail Banking report, BCG says that consumers are now moving to digital channels faster than ever before. In 2020, online banking grew by 23%, and mobile banking jumped by 30%. Analysts believe these pandemic-driven changes will stick and that the migration to digital channels has been accelerated by more than three to four years.

Banks that didn’t keep pace before are falling even further behind, and the door of opportunity for traditional banking is quickly closing. BCG analysts say in an article that the “sun is setting on traditional banking” and the rapid digitization since the pandemic has only increased the vulnerability of incumbent banks. Competition is growing stronger as different players now compete on all stages.

The Essence:

Banks and credit unions can’t afford to waste any more time making changes that merely optimize existing practices. They must reimagine all processes – thinking about what is possible in the digital age.

Even size and financial stability don’t guarantee a competitive edge against the digital disruptors. While governments declared big banks “too big to fail” in the financial crisis, many financial institutions are now “too slow to survive,” BCG observes. “If they are to survive, banks must start acting more like digital giants before digital giants … start acting like banks,” according to BCG.

It’s stuff like this that should make banks “scared shitless,” said JPMorgan Chase CEO Jamie Dimon in January 2021 in response to a stock analyst’s question about sky-high valuations of PayPal, Square and Stripe. In his 2021 letter to shareholders, Dimon noted that financial institutions, including Chase, face extensive competition from both fintechs and big tech companies like Amazon, Apple, Facebook, Google, and now Walmart. “As the importance of cloud, AI, and digital platforms grows,” he wrote, “this competition will become even more formidable. As a result, banks are playing an increasingly smaller role in the financial system.”

( Read More: 7 Essentials of Digital Banking Transformation Success )

The Current Post-Covid Reality

Sure, it’s no surprise that traditional banks have been facing more pressure from fintechs. But BCG notes three post-Covid challenges have only increased the headwinds:

- Global banking revenues won’t return to 2019 levels for at least three years.

- Mobile banking surged 30% during the pandemic and continues to rise.

- Leading retail banks have 2x greater efficiency than the typical retail bank.

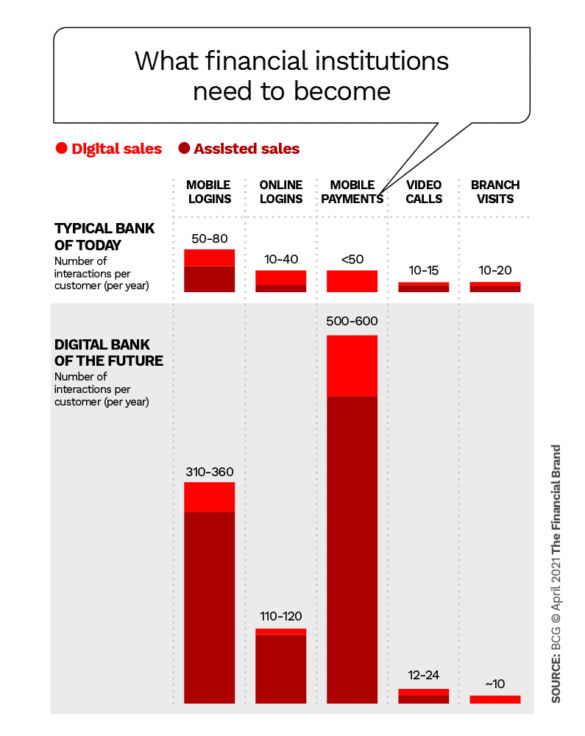

The massive leap in mobile in the past year means a financial institution’s days are numbered if it can’t yet offer the digital functionality that consumers demand. As contactless payments have boomed during the pandemic, half of mobile users are now expected to pay by mobile wallets by 2025. Dig Deeper Within the next year or two, most consumers likely won’t even take a bank or credit union seriously if it lacks basic mobile functionality.

While many institutions have recently engaged in rapid digitization initiatives, many have been efforts to roll out a customer-facing tool. Not many have put sufficient focus on cost control and the back-end processes. Many of these technologies remain tied to physical assets and are difficult to monetize, leaving these institutions at a competitive disadvantage while they try to make up lost revenues.

While a best-case scenario may enable some institutions to make up revenue losses by 2022, a slow recovery with repeated lockdowns and a decline in consumer confidence could drag that out until 2024.

Even for traditional institutions that spent the past few years re-imagining and spiffing up branches, foot traffic is unlikely to ever return to pre-Covid numbers. Due to the sudden shift to digital, BCG expects a net reduction of 26% in the use of branches after the pandemic. “If you have ever said ‘but our branches will be our competitive advantage,’ you might as well sell the bank now. It is a flawed strategy that is about to get worse,” said Chris Nichols, Director of Capital Markets at SouthState Bank.

( Read More: What the Surge in Fintech Launches Signals for Banking’s Future )

REGISTER FOR THIS FREE WEBINAR

Consumer Lending Shakeup

Join a discussion of the new lending landscape and explore proven ways to attract, acquire and retain

Wednesday, May 19th at 2pm (ET)

Front-to-Back Redesign of Value Streams

Despite the cries of doom and gloom, banks and credit unions still have some advantages. “They have the trust of their existing clientele and unique knowledge about their account holders and what they’re doing with their money,” BCG analysts state. In addition, fintechs face regulatory and political barriers that will challenge them for a few more years.

Heads Up:

The day may come when big tech companies can use AI tools to automatically cover all compliance requirements.

Banks and credit unions can find opportunity and even thrive if they focus on the right value streams and digitize and redesign them from front to back. BCG analysts note such a redesign of a value stream can deliver cost reductions of up to 25% and an increase in Net Promoter Score of up to 40%. Redesigning and digitizing these value streams can also improve customer experience and help these banks make up lost ground.

“By breaking the challenge down to the 10 to 15 most important value streams, and by comprehensively digitizing each of these, from front to back, banks can move faster and with fewer missteps,” says Sam Stewart, BCG Managing Director, Senior Partner, and global leader of the firm’s work in retail banking.

Examples of what BCG means by value streams include account opening, securing funds quickly, making it simple to save, optimizing financial well being, simplifying payments, and addressing fraud and service issues efficiently.

The consulting firm advocates an integrated approach with bold business goals rather than incremental improvements. This includes a reimagined customer journey with digital and AI tools that help eliminate work and create a simplified and automated process.

With home buying, for example, most traditional institutions could benefit from more straightforward, online mortgage applications with faster approvals. Digitizing front-end customer interactions in addition to back-end processes would enable half of the applicants to apply online and receive approval in only one hour, according to the report. This could lead to a 15% increase in mortgage settlements and a 25% reduction in the loan’s acquisition cost.

( Read More: Digital Transformation Demands a Culture of Innovation )

Unleashing Digital Sales Potential

Digital sales should be another key area of focus. As it is, many institutions still generate more sales in branches than digitally. Part of this, BCG notes, is that too many banking apps are only designed for processing transactions and accessing account information, not sales. The firm notes digital sales can lead to total sales increases of up to 75% and says some leading banks derive a large portion of sales through digital channels.

Digital sales also involves building a comprehensive database of customer needs. In that way banks and credit unions can use segmentation to help human associates focus on the higher value-added activities, particularly for more complex products.

One leading bank BCG cites is now assigning each of its customers a set of new behavioral lifestyle segments. It then identifies the top three products for each based on an individual propensity score. From there, it creates personalized emails, images, and web templates for mobile, online, and email channels.

This new approach has led to a significant increase in several key metrics, with some products experiencing a 25% increase in purchase rates and purchase value.

( Read More: 4 Tech Trends That Will Massively Transform Banking in 2021 )

The Stacked Operating Model

Building a financial institution’s operations around value streams will enable banks and credit unions to more easily adopt agile ways of working and lead to new levels of digitization. By digitizing the main value streams, says BCG, institutions will fundamentally change the way they operate and fully address cost and control challenges with a model built around new capabilities and ways of working.

This “stacked operation model,” as the firm calls it, will enable an institution’s capabilities to work together more efficiently.

Key Point:

Traditional banking cost structures are no longer sustainable in this non-traditional world.

BCG found that the best financial institutions have 50% fewer employees and operating costs that are 40% lower than that of the typical bank or credit union. These top performers tend to sell higher value products, and more of them, by being less focused on transactions.

"traditional" - Google News

April 28, 2021 at 11:13AM

https://ift.tt/3xx3sqM

Are We Facing an Apocalypse for Traditional Banking? - The Financial Brand

"traditional" - Google News

https://ift.tt/36u1SIt

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Bagikan Berita Ini

0 Response to "Are We Facing an Apocalypse for Traditional Banking? - The Financial Brand"

Post a Comment